Coffee Market 2025: A Price Retrospective

- Igor Bragato

- Jan 23

- 4 min read

2025 stood out as an unusual year of high prices in the coffee market. Following huge global deficits in 2021 and 2024, coffee stayed anchored to historically high prices, while experiencing significant volatility. Overall, 2025 unfolded in two phases: a bear market in the first half that failed to hold, and a bull market in the second half.

Notably, price action reflected a changing mix of drivers, ranging from stocks and positioning to weather and political developments, and understanding these dynamics is ultimately key to putting today’s market into context. In this article, we examine the key forces that drove coffee over the course of 2025, analyzing the main events in chronological order.

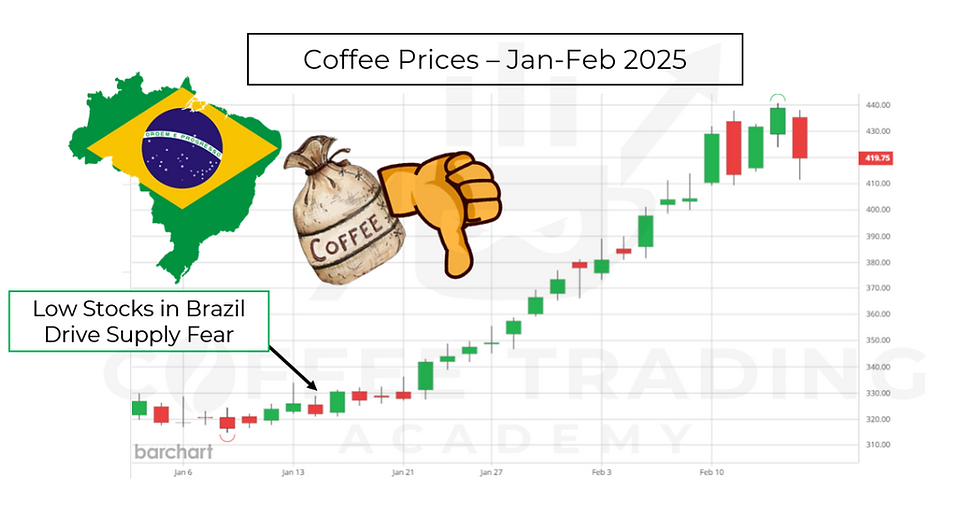

The January Bullish Run

2025 began with a sharp rally in January, driven by supply concerns stemming from extremely low stocks in Brazil. At the time, visible destination inventories were already at historically depressed levels after years of global deficits, and the market was entering Brazil’s off-season, when stocks are typically drawn down.

With the realization that stocks not only were extremely low in destinations, but also in Brazil, supply fears intensified and became a major bullish catalyst that pushed prices significantly higher. Ultimately, coffee rallied sharply from ~320c to ~440c in less than a month.

[Stay ahead of the coffee market. Try our Coffee Research free and get timely insights and analysis.]

At that time, we had the opportunity to directly verify Brazil’s low stock levels by visiting some of the country’s largest warehouses. We rapidly shared these first-hand findings with our clients.

February: The Bearish Reversal

The market stalled near 440c and quickly reversed as the risk shifted toward speculative selling. Managed money had approached the maximum long position, which ultimately left the market vulnerable to the downside via reactionary selling potential.

There was room for spec selling, but it required a trigger. That trigger was the improvement in Brazilian weather, which boosted optimism for the 25/26 crop. Rainfall became more regular and well distributed, in contrast to Q4-2024, and this helped ease the most pessimistic crop forecasts.

[Curious about coffee trends? Sign up for a free trial of our Coffee Research and see the data professionals rely on.]

We visited South Minas twice during this off-season, in November and March. Farmer sentiment had clearly improved by March, and bean size was notably better, with much larger beans compared with the underdeveloped ones seen in late November.

At the same time, Colombian crop flows were strong, as the country harvested a record crop of around 14.8 million bags — the largest in 33 years — exceeding even the most optimistic forecasts, including our own estimate of 14.5 million bags.

May: The Bearish Trend

The price trend turned bearish in May as the new Brazilian crop began to flow and stocks started to rebuild. As the harvest advanced, it became evident that the widespread and severe bean size issues seen in 2024 would not be repeated in 2025, at least not to the same extent. With supply concerns easing and Brazilian stocks replenishing - after having driven the January rally - the market trended lower from May through August.

[Want to make smarter coffee market decisions? Start a free trial of our Premium Coffee Research today.]

August: The Bulls Are Back

Following the Brazilian harvest, the market experienced a sharp and rapid bullish move, pushing prices back toward 400c. This time the catalyst was the imposition of U.S. tariffs on Brazilian coffee, totaling 50%. The U.S. tariffs on Brazilian coffee were a sudden, structural shock to deliverable supply into the U.S.

Once Brazilian coffee became prohibitive, physical buyers still needed coverage and non-Brazil origins were not immediately scalable. In this context, ICE-certified stocks suddenly became the most reliable, tariff-free substitute. That was enough to pull coffee out of certs, which caused a major drawdown in cert stocks.

Notably, cert stocks were already historically low, nearing ~750k bags as of August 2025, and they rapidly declined below 400k bags in the next few months that followed the tariffs. This contributed to intensifying the market inversion, which ultimately reached a record of ~30c in November.

Nov: A Moment of Relief

Later in the year, prices retreated from the 400c highs after the U.S. administration lifted tariffs on Brazilian coffee in mid-November. This move coincided with a slight rebuilding of certified stocks and a broader easing of supply concerns that had dominated earlier in the year. After 12 months of significant price volatility, coffee was ending the year still at high levels.

What Lies Ahead

With U.S. tariffs removed and the next Brazilian crop broadly regarded as large by the market consensus, coffee has entered 2026 under renewed bearish pressure. We will explore the outlook ahead in our next blog - stay tuned!

[Get the coffee market insights you need. Start a free trial and explore our expert analysis and forecasts.]

Comments