What to Expect for The Coffee Market in 2026

- Igor Bragato

- Feb 3

- 5 min read

The coffee market is at a turning point, transitioning from years of tight balances toward a more comfortable supply environment. At present, the inversion is still intense, and destination stocks remain historically low after being depleted by consecutive global deficits that drove high prices.

However, today’s historically high prices will be hard to sustain if the global balance shifts as most expect: a large Brazilian crop is approaching and could drive a meaningful surplus in 2026/27 — potentially the first significant one in many years.

In this article, we break down the main drivers to watch for in the coffee market this year and how they are likely to shape price dynamics. We also explore the main risks that could disrupt the baseline projections.

Context

In our previous article, we examined the key forces that drove prices over the course of 2025, analyzing the main events in chronological order to give context on how the coffee market reached its current position.

[Start a free trial and access our in-depth Coffee Research.]

Ultimately, prices remained high in 2025: coffee ended the year in inversion, and while a more optimistic supply outlook began to form, tight visible stocks and the fear of new weather shocks have kept speculators hesitant to engage in large-scale selling.

It is only now that some bearish pressure has been emerging, as consensus builds around a Brazilian crop reportedly exceeding 70 million bags, which would represent the largest on record.

Brazil at The Center

If Brazil delivers a record crop in the 70-75m million bags range, the market will face an abundance of coffee, significantly reducing the likelihood that today’s historically high prices can be maintained.

Brazil’s coffee crop has an outsized impact on global prices due to its sheer scale, producing roughly a third of total supply.

If this year's consensus proves right, Brazil’s massive volume would outweigh tighter supplies from smaller origins elsewhere. While tracking public estimates for Brazil’s 26/27 crop, we’ve learned that the consensus clusters somewhere around 71-73m bags, made by 47-48m bags of Arabica and 24-25m bags of Robusta, with the most optimistic forecasts even exceeding 50m bags Arabica.

This represents a significant rise over the previous crop, which the industry consensus placed at 62–64 million bags. To put the scale of this increase in perspective, it is roughly equivalent to adding an entire small Colombian crop, such as the 10m bag crop from a few years ago.

The natural follow-up question is whether the estimates are trending lower or higher, as this would indicate how market sentiment - and the narrative shaping prices - is evolving. At this stage, estimates appear to be edging higher, given Brazil’s supportive off-season weather and well-distributed rainfall.

[Try our Premium Coffee Research free and get timely market insights.]

Risks and Opposing Viewpoints

This doesn’t mean that all threats are overcome. The 2024/25 Brazilian crop provides a clear example of how optimism can be misleading after years of weather stress affecting plant physiology. At the time, expectations were for a much bigger crop than what was ultimately delivered, largely due to significant bean defects that only became apparent during harvest.

It follows that the actual Brazil crop will only become clear at harvest, when we can fully assess bean size, quality, and whether farmers are willing to sell in volumes large enough to boost stocks. It also follows that with global stocks being low, any new supply shocks - such as the Brazil crop disappointing - would have an outsized bullish impact on prices.

Ultimately, at Coffee Trading Academy, we are less optimistic than the prevailing consensus. In July 2025, our first survey of the 26/27 season suggested a 73m bag crop, but following dry spells during flowering in Oct-Nov, farmer sentiment shifted more pessimistic and our second survey revised the estimate down to around 69m bags.

This would remain a historically large harvest, yet still significantly below the consensus. As a result, the size of the 2026/27 surplus will largely hinge on which estimate of Brazil’s crop is considered.

The Decisive Moment

This year’s decisive test for today’s elevated coffee prices is likely to come with the Brazilian harvest starting in April–May, when the still-developing large crop begins to translate into actual available supply.

Last year’s Q2 clearly illustrated how Brazil’s new crop flows during harvest can exert downward pressure on prices while replenishing stocks. Importantly, that occurred with a significantly smaller crop of 62-64m bags, which still pressured prices by roughly 25%. Notably, this year we are dealing with a much larger harvest.

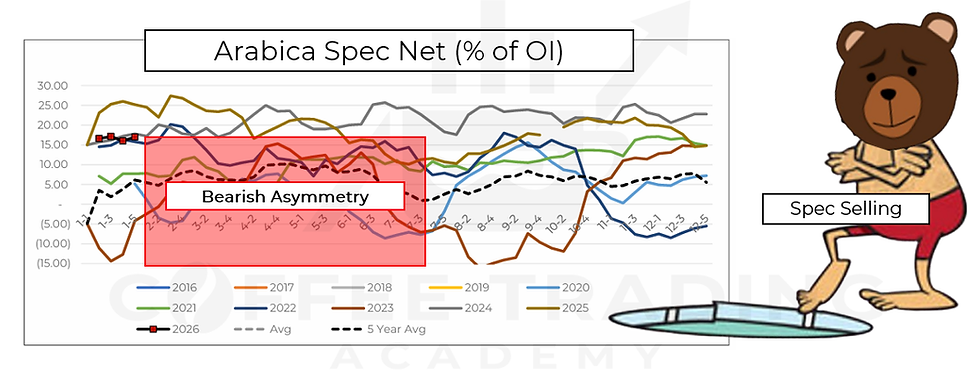

Positioning Asymmetry

Positioning reveals a bearish risk asymmetry, as funds have more room to sell than to buy, having a high long exposure relative to Open Interest. This indicates downside risk, particularly below 340c, where a substantial speculative long position is concentrated. The caveat is that large-scale spec selling is less likely to happen without a clear catalyst, such as large crop flow, selling / producer hedging pressure, stock buildup and/or other events.

[Start a free trial of our Coffee Research and see what you’re missing.]

This does not imply that speculators cannot buy and help support high prices for longer: that’s also a plausible option if the right incentives are in place. It simply underscores a clear asymmetry in risk toward the downside.

The Bulls: Inversion, Stocks and Weather

Up to this point, we’ve highlighted the massive Brazil crop and its potential of reducing prices. However, markets operate in probabilities rather than certainties, and numerous factors could intervene, potentially negating today’s predominant view.

With the bearish case covered, the next question is: what bullish risks should we be watching? The short answer would be the market inversion, the low destination stocks, and weather risks.

The market inversion persists, creating a classic chicken-and-egg problem: for the inversion to break, stocks need to build, but in an inverted market, massive stock buildups are difficult, since there’s a larger cost of holding coffee in destination markets.

We conducted research on the historical relationship between market structure and its underlying drivers, examining the strong correlation with certified stock levels. Typically, when certified stocks are below 1m bags, the market tends to invert, whereas when above 1m bags generally coincide with the inversion breaking.

Certs are currently well under 1m bags (~430k bags), which means there’s a long way to go before we reclaim large-enough levels capable of breaking the inversion. It may take the next Brazil crop (Apr-Aug) to effectively replenish certified stocks in such meaningful way.

Ultimately, the overall low destination stocks may be the Achilles’ heel of the bearish case: if supply falls short of expectations - whether due to smaller crops or farmers holding back supply after recent high prices - stocks could be depleted further, prolonging market tightness.

[Stay informed as the coffee market evolves. Sign up for a free trial of our Premium Coffee Research today.]

If weather disruptions emerge in origins such as Colombia and Central America, they would represent an additional shock to supply.

We’ve been noticing and highlighting to our clients that there’s serious risk of excess rain disrupting harvest and crop flows in Colombia and parts of Central America. Colombia is especially concerning, not only because excess rain has already been confirmed, but also because forecasts point to excessive rain continuing in Feb.

Macroeconomics

The U.S. dollar index (DXY) might continue its descent over 2026, as the United States should cut interest rates at least two more times this year. A weaker DXY tends to support coffee prices, but currency alone is unlikely to sustain prices at very elevated levels if the Brazil crop is big enough to drive a global surplus.

Conclusions

Gradually, market tensions are easing. Supply fears and crowded long spec positioning become increasingly difficult to defend. This does not necessarily mean the move is fully complete, but it does mean there are materially fewer arguments for keeping the market at extremely high levels. Unless another supply or weather shock emerges this year, the sustainability of super-high prices appears less likely.

[Sign up for a free trial of our Premium Coffee Market Research!]

Comments