Coffee Report Focus 3: Open Interest

- Ryan Delany

- Aug 31, 2021

- 4 min read

Updated: Nov 23, 2021

One of the reports that serious traders look at on a daily is the Open Interest reports. This report gives rapid insight into whether the previous day's price action was driven by expanding or contracting interest in the commodity.

We'll look at what that means on a practical level, and how we can use this to predict price action, but let's start with some context.

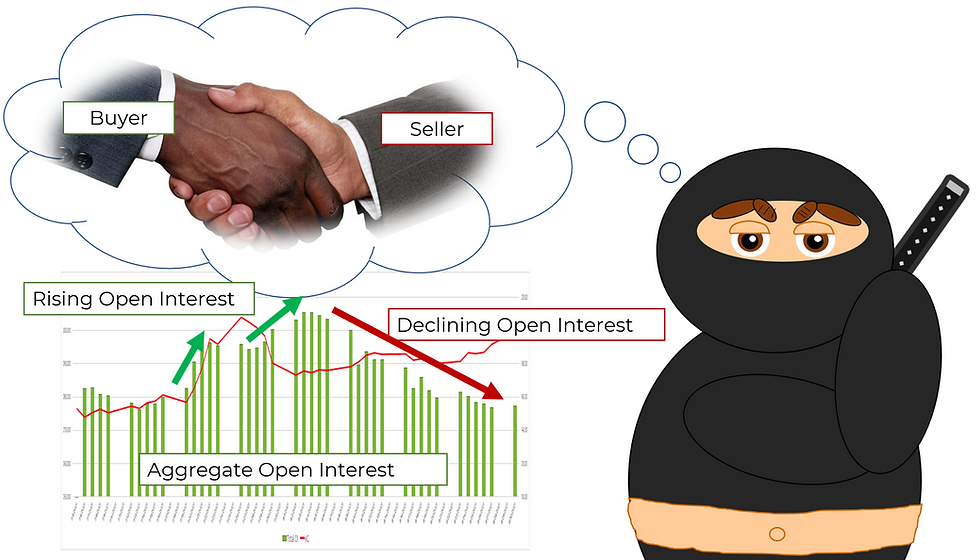

For Every Buyer, a Seller:

The Open Interest (OI) shows how many contacts are open for a given future. One of the fundamental features of futures contracts is that they are bilateral--for every buyer, there must be a seller. Whenever a trade is executed on the screen to buy a future, there is another person on the other side who has just agreed to sell it.

When neither party owned a contract before a trade is executed, then 1 lot of open interest is created. As more traders join the contract and open more positions of long and short futures, more open interest is created. This is rising or increasing open interest.

Rising vs Declining Open Interest

However, there are two other possibilities: if two parties hold opposing sides of open positions they can opt to trade to close those positions out. When the owner of a future sells their long position, and the seller of the future buys back their short, then 1 lot of open interest is closed and open interest declines (decreases).

The third and final possibility is that if one person closes out their position (Long sells a future) and the other person puts on a position (flat position goes Long) then the open interest remains flat.

So the three possibilities for every trade are as follows:

1. open interest goes up (more futures contracts open)

2. open interest goes down (less contracts open)

3. open interest stays flat (same contracts open)

At the end of each day, the exchange sums the total number of contracts open for each futures month, and this is the open interest reported.

Aggregate vs Individual OI:

Usually when we talk about Open Interest, we are referring to Aggregate Open Interest, but its important to note that each futures month has its own Open Interest. When all contracts are added together, it is referred to as Aggregate Open Interest.

Both of these are useful to know for a trader. Individual contract OI is especially useful for ensuring liquidity before first notice day, and noting which contract is generally regarded as the spot contract.

In the below table from my weekly report, you can see that on Aug 2nd, September (KCU21) was the spot contract, but by Aug 16th, December (KCZ21) had become the liquid front month contract. By Aug 30th (well into Notice Period), there are only 61 lots left of Open Interest outstanding in KCU21.

The individual months are are also useful to look at, to see which of the back months are being traded by specs and the trade. For example, in the chart below, we can see that the Dec 22 contract (KCZ22) has more OI than any of the other back months. This suggests that it is being traded more heavily than the others and probably has better liquidity.

Open Interest by Cover Month

Making Sense of the Price Action:

On a practical, daily basis, looking at OI gives us important information about the preceding day's price action. It tells us whether the day's trading was dominated by traders opening or closing positions. This is most relevant when talking about the speculator.

We generally assume that the spec is driving price action. This isn't always the case, but it often is for a good reason. The spec is not hedging, so when they trade, they usually need to be more aggressive in putting on positions and they may even find it desirable to move the market (buyers want prices to rise).

The commercial by contrast is hedging physical positions, and since they are hedging they do NOT want to move the market (sellers want prices to rise, not fall). This means that they are usually more patient and deliberate when putting on positions. So when prices are moving it is usually driven by the spec putting on or taking off a position.

With the above information, and assuming that the spec is driving price action, we can then look at the change in OI and make 4 very broad assumptions:

1. When OI goes up and price goes up, specs are adding longs.

2. When OI goes up and price goes down, specs are adding shorts.

3. When OI goes down and price goes up, specs are covering shorts.

4. When OI goes down and price goes down, specs are selling longs.

Open Interest and Price Matrix

As short hand, people will often say "new shorts", when OI goes up and price goes down but really they mean "new spec shorts".

This information is particularly important depending on how the Spec is positioned in the COT. In my blog on the COT, I talked about the two different ways to interpret spec positions but essentially we are looking for a low spec position who will add more, or a high spec position who will liquidate. The OI will give us hints as to whether this is starting to happen and the COT will let us know how much potential their is to move.

Anticipating the COT:

This brings us to the final use for OI. By using the matrix above, we can try and anticipate what the COT will show. Since the market prices often resets to any big moves in the COT, market participants often use the OI reports to try to anticipate what the COT will show.

I've seen traders try to calculate directly what the COT will be using the above method. Feel free to try it out and see how accurate your estimates are.

Final Thoughts"

The above methods I've outlined are some of the more "traditional" methods of looking at Open Interest. They are useful, for keeping pace of the market, avoiding surprises and being able to talk intelligently with other traders about what is going on. However, the real edge will come from looking at the market intelligence in new and creative ways.

Would love to hear if any of you have other ways to look at OI, or any new ideas on how we can use this information. Feel free to email me or comment below if you want to add to the conversation!

Comments