Cocoa Grinding Differences Across Regions – Part 2

- Diego Miranda

- Mar 12

- 6 min read

In the first part of the Grinding Differences Across Regions blog series, we explored the mechanics of the European and Asian grinding hubs, the way both operated, and the differences between them. Through this lens, we understood how each region reacted to the 2024 cocoa rally and the subsequent price decline.

For the second part, we will analyze the third and last region among the three most well-known cocoa grinding associations, ECA, CAA, and NCA. Beyond that, we will also look into Ivory Coast's processing figures, which, besides being the world’s largest cocoa producer, also plays an essential role in the processing markets – a role that has potential to expand in the future.

North America Persistence Going in the opposite direction of Europe and Asia, North America presented the best results in 2025, to the point of increasing its grinding figures in some quarters. These results suggest that its markets present a far more resilient structure, even in extreme situations such as those seen in the last few years.

[Want better cocoa market insight? Start a free trial of our Cocoa Research and get access to expert analysis and key market data.]

Once again, a matter that deserves emphasis is hedging. While Europe locks in a considerable amount of its bean prices in advance, and Asia is somewhat lacking in this matter, North America is by far the region that uses this practice the most.

It is estimated that North American companies hedge over 70% of their cocoa in advance, meaning that chocolate prices rose far more smoothly, spreading the increases throughout 2024 and 2025 instead of concentrating them in a few large hikes.

At the same time, US consumers were able to show more resilience than their counterparts in other regions. Unlike Europe, North American economies, especially the US economy, have shown above-expected growth in the last quarters of 2025, which is likely to have helped consumers deal with the higher costs. And unlike in Asia, sweets consumption is a well-established part of American culture, meaning consumers are less willing to give up their chocolate, even if they have to pay a higher price for it.

Combined, these factors led North America to present the best cocoa grinding numbers in 2025. Although Q1 started with a 3.0% drop, this figure was already reduced to 2.8% in Q2, while Q3 and Q4 even presented YoY growth of 3.2% and 0.4%, respectively. Although these figures were not enough to save the whole year, since processing still fell 0.6%, they were far less severe than the impacts seen in Europe and Asia.

Caveat Despite the good results, there are still a few elements we must remember about North America’s situation.

The first is that this is by far the smallest processing region, representing around 30% and 50% of European and Asian cocoa grinding, respectively. As a result, even though North American figures were far above those of the other two regions, their overall influence on global demand is significantly smaller compared to other regions.

[Curious what’s driving cocoa prices? Try our Cocoa Research free and stay informed on supply, demand, and market trends.]

The other element concerns the data collection itself. The North American grind number is based on reporting processors, and the industry has a smaller set of large players compared with Europe’s broader processing ecosystem. That concentration can make the series more sensitive to changes in reporting coverage or operational decisions by a few firms.

In 2025, YoY comparisons were affected by changes in the reporting base, as more processing facilities were added. It is likely that these changes increased grinding figures, although we cannot attribute the whole positive result to this change.

Ivory Coast Besides Europe, Asia, and North America, West Africa also constitutes a relevant player in the global cocoa processing industry. In the region, Ivory Coast once again occupies the main spot; not only is it the world’s largest cocoa producer, but it is also in the race to be the biggest processor, competing with the Netherlands for the first spot.

Unlike the other regions, we have access to the Ivorian monthly grinding figures, provided by the Coffee and Cocoa Exporters Association (GEPEX). Therefore, we can have an even better idea of how processing developed throughout 2025.

Ivory Coast was actually more capable of enduring the initial shock caused by the rally, as its processors tend to forward sales directly from the Conseil du Café-Cacao (CCC), meaning they did not suffer the impact of high prices as quickly. At the same time, increasing grinding figures has been a strategy of the Ivorian government for a few years now. To support its objectives, the government uses a series of measures, such as providing preferential access to beans for local grinders, financing lines coordinated by the CCC and development banks, and structured trade finance arrangements through international banks, all of which were amplified during the shortage.

[Looking for reliable cocoa market research? Sign up for a free trial and see what our Cocoa Reports include.]

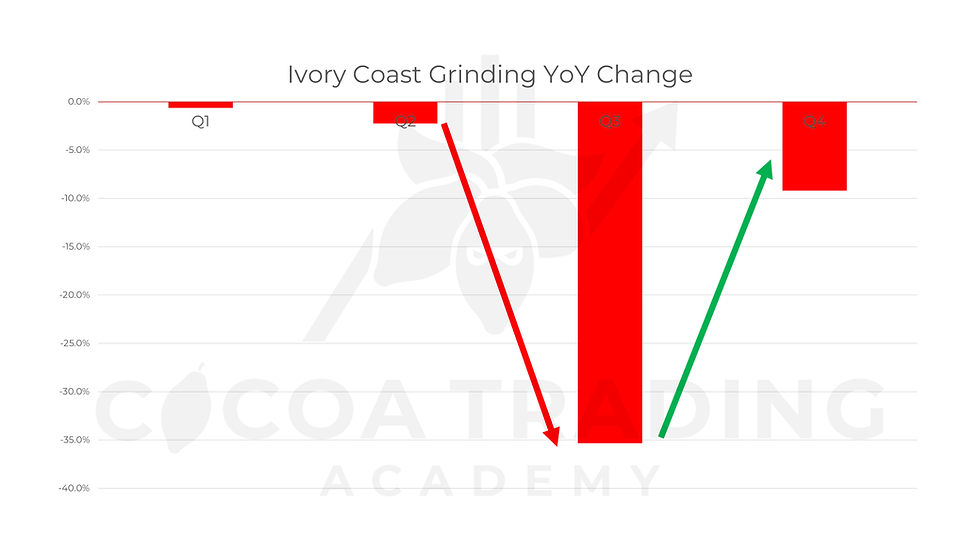

As a result, cocoa processing in the first quarter fell by only 0.6%, pulled down by drops in January and February, while March even showed 5.6% YoY growth. The situation worsened slightly in Q2, as grinding dropped 2.3%, but remained far better than what we saw in Asia and Europe.

The Reversal The calm waters could not last forever, though, and a storm was brewing on the horizon. The third quarter brought with it a severe hit to Ivorian processors, as the forward sales they had previously made came to an end, and processors now had to deal with market reality. Along with that, the internal cocoa supply had become far scarcer, as the 2024/25 main crop had already ended, and the mid-crop proved to be far worse than early forecasts had indicated.

In a worse market situation and unable to secure their beans, grinding figures collapsed between July and September, falling 35.3% YoY in the third quarter of last year. Such an outcome was not only worse than anything seen by the other regions, NCA, ECA, and CAA, but it more than doubled the drop seen in the Asian hub, which had already appalled the markets with its intensity.

To Live for Better Days Intense as it was, the Ivorian catastrophe proved to be short-lived. Although October grinding still presented a 25.4% YoY drop, it was already considerably better than what was seen in Q3.

The situation continued to improve in the following months, with November falling only 6.6% and December even growing 3.6%. In the end, Q4 processing figures fell by 9.2%, almost four times less than in the previous quarter.

[Follow cocoa markets with more confidence. Start a free trial of our Cocoa Research and get timely market insights.]

The recovery was supported by the beginning of the 2025/26 cocoa crop, which mitigated the supply shortage problems seen during the previous mid-crop. Even though the opening of 2026 was not so positive, as processing in January fell 2.1%, the number is still in line with what is usually seen for the month, suggesting the worst has come to pass.

Looking Forward Expectations are mixed regarding the future of cocoa grinding. On one hand, cocoa prices continued to collapse in 2026, falling below $3,000/MT for the first time in almost three years. Combined with this, cocoa supply itself has increased, supported by both a partial recovery in West Africa and the fast growth of Latin America, meaning companies will not have much trouble securing beans, which was sometimes a problem even when processors were willing to pay the necessary prices for them. Both factors should help increase grinding figures in the short term.

On the other hand, many companies still have hedged beans at higher levels, meaning it will take a while for the $3,000/MT level to become completely real for the industry. At the same time, the fact that prices have come down does not mean that the rally will have no effects moving forward.

To deal with the shortage, companies had to make all kinds of changes in their structure and supply chains, finding new cocoa sellers and chocolate buyers, changing the recipes of their products, and updating their machinery; many were unable to deal with the pressure and simply closed their doors for good. Just because prices have come down does not mean everything will return to the way it was before.

Considering both sides of the situation, it is reasonable to assume that the grinding recovery will be a long and hard process. Although 2026 should be better than what we saw in 2025, we cannot expect cocoa consumption to simply return to the way it was prior to the historical shortage.

That said, cocoa markets operate in probabilities rather than certainties. What appears reasonable does not always materialize, and the past few years have shown this, while cocoa has been one of the most volatile and unpredictable of the soft's commodity markets.

[Get a clearer view of the cocoa market. Explore our Cocoa Research with a free trial and see the value for yourself.]

Comments