Rallying Physical Prices and Its Implications for Coffee

- Igor Bragato

- Apr 30

- 4 min read

Coffee differentials have surged across distinct origins and varieties this year, especially so in Brazil, where past crops are being offered at multi-year highs in the physical market. This has effectively disrupted the build-up of ICE certified stocks, as differentials are not only far too high to justify delivery to the exchange, but also incentivize consumption of comparatively cheaper certified inventory. If unchecked, this draw down in certs could lead to rallying in the spreads and futures.

In this article, we will discuss the drivers behind it, the specific dynamics unfolding at origin level and the implications of the rally in diffs.

Source of the Differential Rally

We have seen the rally in differentials but why did diffs rally in the first place?

From Discounts to Premiums

There are two primary factors that typically drive physical prices: the futures market and local S&D dynamics in origin.

The most recent catalyst behind the rally in differentials was the sharp selloff in coffee futures in Jan, with a 60c drop rapidly lifting the bid for the physical markets. While futures fell, the Oct harvests wound down, reducing new crops flows from Centrals, Colombia, Africa and Vietnam.

[Stay ahead of the coffee market. Explore our Coffee Research plans for regular insights on supply, demand, and pricing.]

So ultimately, from a broader perspective, differentials were rallying on the back of two concurrent forces: falling futures and reduced new crop flows. That’s the broader explanation, but if we analyze things at origin level, there’s more nuance to it.

Brazil: Past-Crop Retention

The sharpest rise in differentials was in Brazil, where past-crop coffee shifted from discounts or small premiums (back in Jan) to multi-year highs of +20c to +30c within weeks. There wasn’t a single driver behind this, but rather, it seemed to be the result of competing forces at play.

Once coffee prices fell (relative to Q4-2025), farmers lost their selling appetite. Afterall, being well capitalized from years of historically high prices, why sell coffee at much lower levels than what they had grown accustomed to? Instead, they held on to the coffee for higher prices.

Meanwhile, logistical bottlenecks formed at ports, and some exporters opted to delay shipments. Nothing too unusual, but it further contributed to tightening nearby availability and bid diffs higher. Ultimately, the low exports combined with firm diffs seem to imply real nearby tightness.

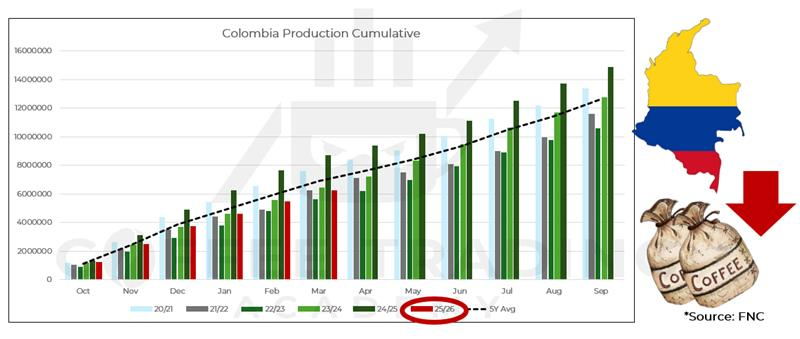

Colombia: Small Crop

Colombian coffees are trading at a +45c premium, and that seems consistent with reduced new crop flows. Colombia’s 25/26 crop has underperformed so far, with cumulative production falling below expectations (already modest, after last year’s multi-year record output) and well under the 5-year average.

[Looking for consistent coffee market updates? Our Coffee Research plans deliver expert analysis straight to your inbox. Sign up for a FREE trial today!]

Alongside the wide selloff in the futures market, this helps explain the currently elevated differentials. The caveat in Colombia’s case is that, although diffs have rallied, they remain well below the ~70c peaks seen during the 2022 supply crisis. That’s a contrast to Brazil, where diffs have reached multi-year highs.

Central America: Demand Pulling Supply

In Central America, particularly Honduras, firm differentials (Milds near 30/40c) combined with strong exports suggest that demand is actively absorbing available new crop supply.

The data for Honduras is particularly striking: cumulative 25/26 exports (Oct-Mar) have reached 3 million bags, the highest in recent years. For context, this represents a 47.5% increase over the 5-year average and a 54.9% increase vs the same time in last season.

Even though Honduras is coming off a large 25/26 crop (which typically supports higher exports), the record export figures are noteworthy and suggest a strong demand pull, with buyers sourcing Central American coffees while Brazilian coffee is expensive and availability is reduced.

First Order Impact: The End of Certs Build

The most immediate impact of the rally in diffs was something that we anticipated to clients of our premium reports, which is the interruption of the increase in certified stocks.

The reason is simple: the Feb certs build-up was largely fueled by coffees that were economically viable for certification in Jan (especially from Central America), but that’s no longer the case.

[Get the data behind coffee price moves. Our Coffee Research plans provide clear, timely market analysis. Check out our Premium Research Plans.]

With differentials trading at substantial premiums across the board, the economic incentive to certify vanished.

To make matters worse, the high diffs instigate sourcing from certs as a cheaper alternative to physicals. Certified inventory can be attractive coffees to buyers on multiple fronts. Notably, past crop washed coffees are often used as Brazil replacements in roaster blends, so when Brazil differentials are rich, we see certs used as Brazil replacements.

We can also see past crop certs be used to dilute expensive uses of specific origins. If a particular blend requires Honduras or Colombian coffee for example, a past crop of the same origin could replace up to 10% with minimal impact on a commercial blend.

Thus, high differentials have been a major catalyst for the recent drawdown in certs (-55k bags MoM).

Second Order Impact: Market Inversion

A second-order effect is the maintenance and extension of the calendar spread inversion. Low certified stocks are closely correlated with inversions in times of market scarcity. The certified inventory is well below 1,000,000 bags which signals a scarcity environment, and in these environments the market will invert exponentially as the certified stocks draw down to prevent a draw down to 0.

We have seen this dynamic play out recently. Notably, when certs were rising in Feb, the inversion lost much of its intensity and fell to only a few cents (+2/4c by Feb 19th) in the front month contracts. By contrast, once the buildup stopped and certs got consumed, the inversion intensified again, with front-month contracts up to current levels of +15c.

Conclusion

Ultimately, differentials have rallied according to the two primary drivers of physical prices: futures market and local S&D dynamics. In this case, the rally in physicals was driven by a double whammy of a futures market decline in anticipation of the large 26/27 Brazil crop, plus a shortage of available coffees in the present. While it is typical to have a low-point in stocks before the Brazil harvest, we are coming from an atypically low starting point. This has led to a drawdown in certs and a particularly forceful impact on calendar spreads.

[If you enjoyed this, you'll love our Premium Coffee Research. Redeem your free trial here.]

Comments